13 November 2020

Tougher restrictions drive pub and restaurant group sales into reverse

Total Like For Like Sales Growth

The roll-out of more regional COVID restrictions further depressed sales in Britain’s managed pub, restaurant and bar groups in October, latest data from the Coffer Peach Business Tracker show.

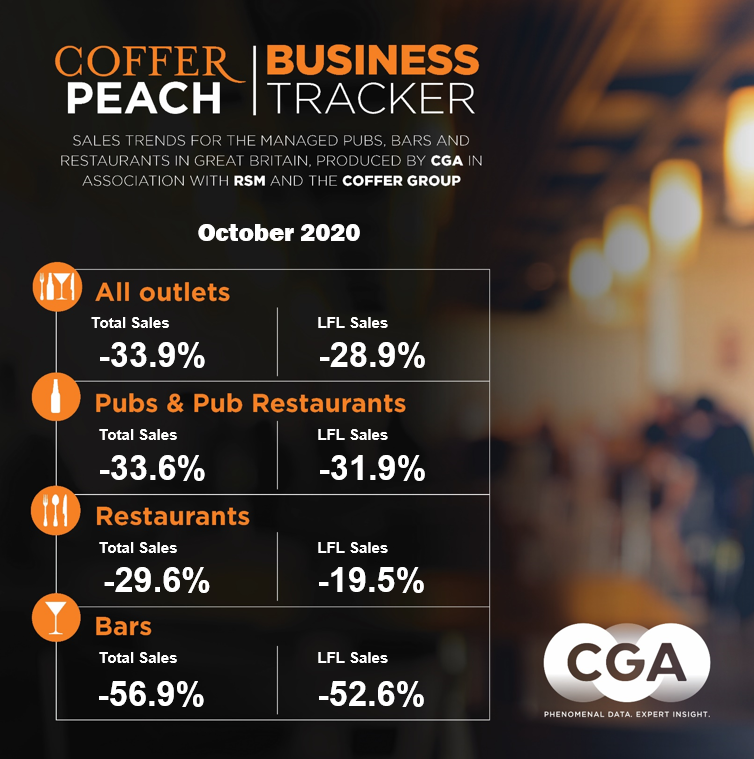

With 83% of group-owned sites open, down from 88% in September, total sales across the whole managed sector were down 33.9% on the same month last year, a clear deterioration from September when sales were 20.3% below 2019 levels and August when they were just 12.2% down.

All parts of the market performed worse than in September. Like-for-like sales in those businesses trading were 28.9% below October last year, compared to a 14.7% fall in September.

“Drink-led pubs and bars have been particularly badly hit, and with England now in full-lockdown, you can only wonder how many will re-emerge in their current state, how many will have to revamp their trading styles, including switching their emphasis to food?” said Karl Chessell, director of CGA, the business insight consultancy that produces the Tracker, in partnership with The Coffer Group and RSM.

“What’s crystal clear is that even before total lockdown in England, the imposition of Tier 2 and 3 restrictions across large swathes of northern England, as well as the tough restrictions in Scotland and Wales, had a massive negative impact on sales performance.” added Chessell.

Drink-led pubs saw total sales down 37.6% and like-for-likes down 35.3% on October last year. Corresponding figures in September were minus 22.7% and minus 21.1%. Food-led pubs and pub restaurants fared a little better, but still performed markedly worse than in September, with total sales down 28.9% and like-for-likes down 27.8%. Across all managed pubs food sales were down 24.5% with drink sales dropping 37.6% on the same time last year.

Restaurant groups performed the best, helped by the cut in VAT on food and delivery sales, but still saw total sales down 29.6%, and like-for-likes 19.5% below October 2019. Delivery accounted for 12.3% of sales among restaurant groups over the month, up from 10.4% in September and the pre-lockdown level of 5.9% in February.

Regionally, London continued to struggle. Total sales across managed pubs, bars and restaurants inside the M25 were down 39.5%, compared to 32.1% in September, with collective like-for-like sales in those sites open down 35.0%. Outside the M25 the market saw like-for-like sales down 26.8% and total sales down 31.9%.

Bar groups had the worst of the month, with like-for-like sales down 52.6% and total sales down 56.9%.

At the end of October, underlying annual like-for-like sales for the whole market were down -26.2% on the previous 12 months, with total sales down -37.9%.

David Coffer, Chairman, The Coffer Group, said, “If anything, October’s figures were better than many feared. The pressures on the hospitality sector to keep businesses going during lockdown is immense and the industry has been as creative as possible. Crucially, we will be concerned about how the public will react to the lifting of the restrictions in December – will their eating and drinking habits have culturally changed? The post lockdown figures especially over Christmas are sadly or joyfully going to be the acid test for the Industry. We expect it will be a truly seismic period with far reaching effects.”

Paul Newman, head of leisure and hospitality, RSM, said “It is impossible to put a positive gloss on such depressing results in the last full month of trading prior to England’s second lockdown. This week’s news about an imminent vaccine is just the fillip the sector needs as operators turn their focus to the operational challenges of successfully re-opening their businesses on 3 December for the truncated, but ever more crucial, festive trading period. I’m amazed at the creativity shown by operators to stay in business during lockdown and I urge consumers to support their local pubs and restaurants over the coming weeks. A whole business eco-system is reliant on their support – from suppliers to operators and landlords.”

A total of 56 companies, with between them 9,295 sites open for business, provided data to the October Tracker.

Participating companies receive a fuller detailed breakdown of monthly trading. To join the cohort, contact Andrew Dean, Andrew.Dean@cga.co.uk

About Coffer Peach Business Tracker

CGA collected sales figures directly from 56 out of the 59 leading companies participating. Participants include: Amber Taverns, Azzurri Group (Ask Italian, Zizzi), Banana Tree Restaurants, Beds and Bars Ltd, Big Table Group (Bella Italia, Las Iguanas), Bills Restaurants, BrewDog plc, Buzzworks Holdings Group, Byron, City District Enterprise (Fazenda), Coaching Inn Group, Cote Restaurants, Deltic Group Ltd, Dominion Hospitality, Drake & Morgan, Fuller Smith & Turner, Gaucho Grill, Giggling Squid, Greene King (Chef & Brewer, Hungry Horse, Flaming Grill), Gusto, Hall & Woodhouse, Hawthorn Leisure, Honest Burgers, Laine Pub Co, Le Bistrot Pierre, Loungers, Marston’s, McMullen & Sons Ltd, Mitchells & Butlers (Harvester, Toby, Miller & Carter, All Bar One), Mowgli, Nando’s Restaurants, New World Trading Co, Oakman Inns, Peach Pubs, Pizza Express, Pizza Hut UK, Prezzo, Punch Pub Co, Restaurant Group (Frankie & Bennys, Chiquitos, Brunning & Price), Revolution Bars, Rileys, Rosa’s Thai, Snug Bar, St Austell, Star Pubs & Bars, Stonegate Pub Co (Slug & Lettuce, Yates’, Walkabout, Bermondsey Pub Company), TGI Fridays UK, The Alchemist, True North Brew Co, Upham Pub Company, Various Eateries (Strada, Coppa Club), Wadworth & Co Ltd, Wagamama, Whitbread (Beefeater, Brewers Fayre, Table Table), YO! Sushi and Youngs.

Recent Reports:

- Pub and restaurant groups suffer sales set-backs in September

- Food-led pub and restaurant groups get August sales back on track

- Pub and restaurant groups see sales halved in first month back

- Out-of-home food and drink sales fall nearly 60% in March

- Out-of-home food and drink sales down 3.3% in February

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}