15 January 2021

Christmas sales misery for pub and restaurant groups

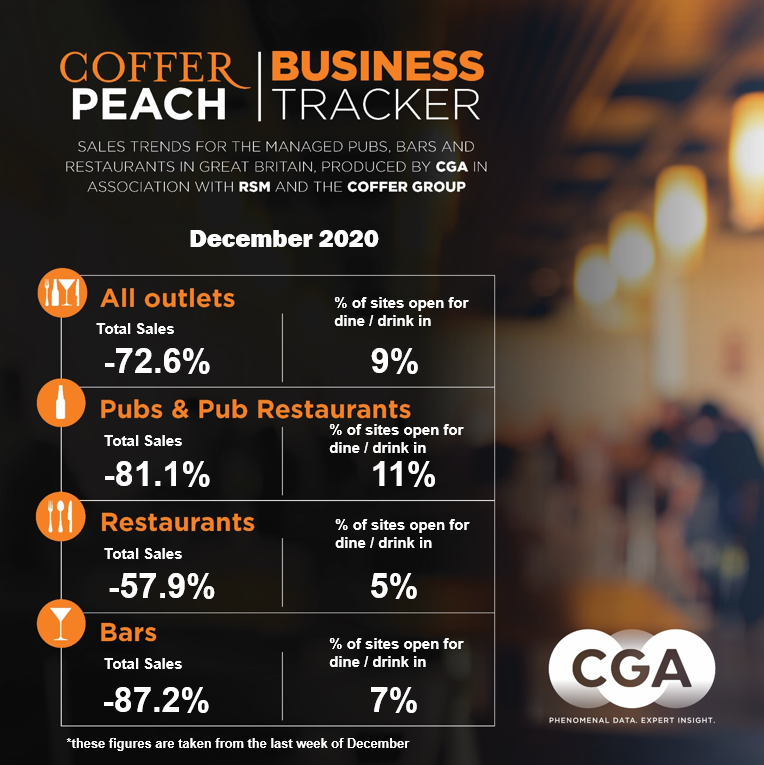

Total Like For Like Sales Growth

Britain’s managed pub and restaurant groups saw total sales drop by 72.6% over the festive season, in what should have been the sector’s busiest trading period of the year, latest data from the Coffer Peach Business Tracker show.

“Hopes that Christmas and New Year would help at least part of the market recoup a little of the income lost earlier in 2020 were dashed when the Government started to impose increasingly severe tier restrictions across England in the run-up to the Christmas break, with further prohibitions for New Year, on top of the restrictions in place in Scotland and Wales,” said Karl Chessell, director of CGA, the business insight consultancy that produces the Tracker, in partnership with The Coffer Group and RSM.

Trading figures for the five weeks from November 30 to January 3 show that drink-led managed pubs and bars were worst hit, with total sales down 83.7% and 87.2% respectively on the same period last year. Managed food-led pubs and pub restaurants were down 78.2%, while group-owned restaurants saw total sales drop 57.9%.

“Restaurants had a marginally less miserable time, benefitting from people out Christmas shopping at the start of month and more importantly from delivery business. Overall in December, delivery accounted for 23% of restaurant chains’ sales,” added Chessell.

Regionally, London, which was largely open at the beginning of December, also fared slightly better than the rest of the country with sales down 66.8% on last year, compared to 73.9% down outside of the M25.

“The tier system had already kept pubs and restaurants across large parts of the country closed from the start of the month, but the escalation of measures saw the sector effectively grind to a total standstill by the end of December, even before January’s return to complete lockdown,” observed Chessell.

At the beginning of the festive period Tracker figures show that just over half of the country’s managed pubs, bars and restaurants were trading again after November’s lockdown. By the end of December the number was less than 10%.

At the end of December, underlying annual sales for the whole market were down 50.5% on the previous 12 months.

David Coffer, chairman of The Coffer Group, said “It doesn’t need a genius to work out why these dreadful trading figures have materialised. The big question is how do we come out of the spin? With most operators now unable to create any turnover whatsoever the accrual of debt has become critical. The crucial date will be 31st March when the Moratorium for insolvency is removed and many operators will face over a year of unpaid property outgoings which landlords will be able to aggressively pursue. Similarly, there are debts relating to rates, taxes, VAT, insurance and repayment of business loans. Altogether a tsunami of debt which needs to be dealt with from a standing start. How our sector, and indeed others, manage this predicament will be more than a challenge.”

“All operators have been endeavouring to conserve resources by furloughing staff and closing their premises but it will be exceptionally hard to “open the doors” and just start trading. Customer confidence, cultural changes, unemployment, and lack of spending power will have an impact certainly in the years following. There will be opportunities for those who wish to expand with grateful landlords and helpful banks involved. We all hope for additional Governmental intervention come April but come what may this is not the landscape that any of us could have imagined let alone experience. I don’t expect these operational figures to improve in any way over the coming quarter but I have the greatest hope that the spirit to survive and thrive will come to the forefront.”

Paul Newman, Head of Leisure and Hospitality, RSM, said “December’s results lay bare the stark reality facing the hospitality sector. The government’s tier restrictions led to most sites shuttering early in the month, compounding pressure on costs with operators already committed to serious outlays with suppliers to meet anticipated festive demand. With new year lockdown measures unlikely to be lifted before Easter – in an optimistic scenario – the hospitality industry is left facing its greatest challenge yet. Businesses and their funders desperately need greater visibility to support their cash flow forecasting. It’s hard enough to predict when top line income will return without the ongoing uncertainty around costs. Urgent clarity on substantial, additional Government support is needed now as the 3rd March Budget may simply be too late. The Chancellor’s latest grant package does not go far enough, barely touching the fixed monthly site costs that businesses face. At the very least, a further year of Business Rates relief and the extension of the 5% reduced VAT rate would provide some hope for the future and allow more companies to emerge the other side of this pandemic to fight another day.”

A total of 51 companies provided data to the December Tracker.

Participating companies receive a fuller detailed breakdown of monthly trading. To join the cohort, contact Andrew Dean, Andrew.Dean@cga.co.uk

About Coffer Peach Business Tracker

CGA collected sales figures directly from 51 out of the 60 leading companies participating. Participants include: Amber Taverns, Azzurri Group (Ask Italian, Zizzi), Banana Tree Restaurants, Beds and Bars Ltd, Big Table Group (Bella Italia, Las Iguanas), BrewDog plc, Buzzworks Holdings Group, City District Enterprise (Fazenda), Cote Restaurants, Dominion Hospitality, Drake & Morgan, Fuller Smith & Turner, Gaucho Grill, Giggling Squid, Greene King (Chef & Brewer, Hungry Horse, Flaming Grill), Gusto, Hall & Woodhouse, Hawthorn Leisure, Honest Burgers, Laine Pub Co, Le Bistrot Pierre, Loungers, Marston’s, Mitchells & Butlers (Harvester, Toby, Miller & Carter, All Bar One), Mowgli, Nando’s Restaurants, New World Trading Co, Oakman Inns, Peach Pubs, Pizza Express, Pizza Hut UK, Prezzo, Punch Pub Co, Restaurant Group (Frankie & Bennys, Chiquitos, Brunning & Price), Revolution Bars, Rileys, Rosa’s Thai, Snug Bar, St Austell, Star Pubs & Bars, Stonegate Pub Co (Slug & Lettuce, Yates’, Walkabout, Bermondsey Pub Company), TGI Fridays UK, The Alchemist, Upham Pub Company, Various Eateries (Strada, Coppa Club), Wadworth & Co Ltd, Wagamama, Whitbread (Beefeater, Brewers Fayre, Table Table), YO! Sushi and Youngs.

Recent Reports:

- Drink-led pub and bar groups suffer 90% sales drop across November

- Tougher restrictions drive pub and restaurant group sales into reverse

- Pub and restaurant groups suffer sales set-backs in September

- Food-led pub and restaurant groups get August sales back on track

- Pub and restaurant groups see sales halved in first month back

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}