1 July 2021

Rolling 12-month sales down 27%, but June provides cause for optimism as sales near 2019 levels

Total Like For Like Sales Growth

- Coffer CGA Business Tracker reveals 1% drop on June 2019 amid COVID restrictions and other challenges

- Restaurants’ sales in growth but pubs, bars and London in the red

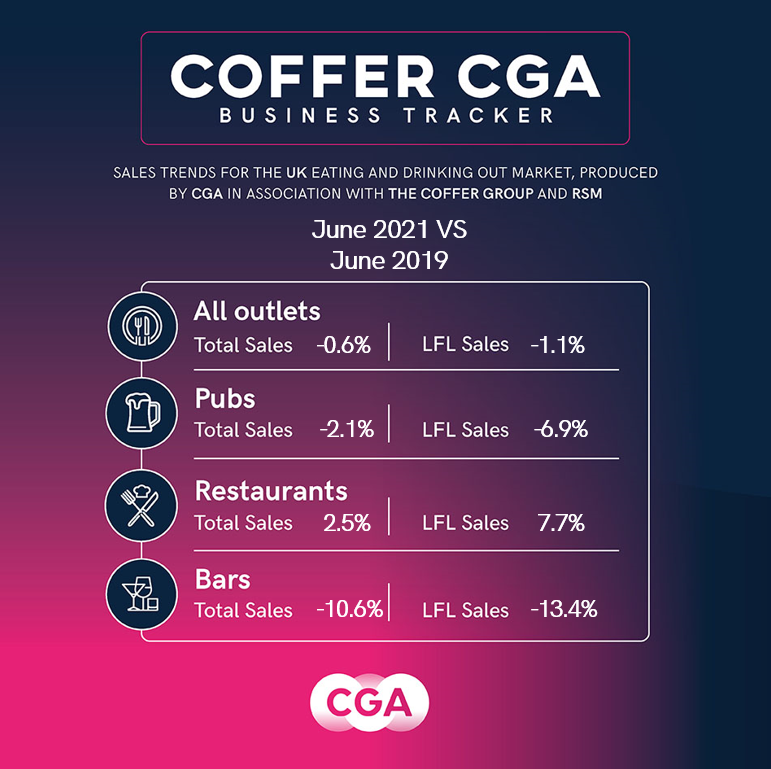

Britain’s managed pub, restaurant and bar groups saw sales drop just 1% in June from the same month in 2019, the new edition of the Coffer CGA Business Tracker reveals.

The Tracker, produced by CGA in partnership with The Coffer Group and RSM, shows sales were nearly level on both a total and like-for-like basis. Consumer demand was particularly strong in restaurants, where total sales were up by 3% in June. Pubs recorded a 2% drop, with mixed weather and restrictions dampening any benefit from the Euro 2020 football tournament. Sales were down by 11% in bars, where social distancing and early closing requirements continue to impact footfall.

June’s performance is a significant improvement on May, when total sales were down by 26% on May 2019. The Tracker indicates a particularly good month for regions beyond London: sales outside the M25 were up 4% in June, but down by 11% inside the M25.

Many operators continue to benefit from strong delivery and takeaway sales, which CGA’s separate Hospitality at Home Tracker shows have more than tripled from pre-COVID levels. Higher average spend by some consumers after the end of lockdown also contributed to the solid month.

However, the Tracker also confirms the lasting impact of the pandemic on hospitality, with managed groups’ sales in the 12 months to June 2021 down by 27% on the previous 12 months. Research for the CGA and AlixPartners Market Recovery Monitor meanwhile shows that Britain now has around 9,000 fewer licensed premises than it did a year ago.

Karl Chessell, director – hospitality operators and food, EMEA at CGA, said: “June’s figures are testament to the enduring appeal of restaurants, pubs and bars and the resilience of the businesses behind them. With an easing of COVID restrictions imminent, it suggests a bright outlook for the eating and drinking out sector. However, rising costs and limited capacity mean many businesses are still struggling to make a profit, and major challenges including debt burdens and a recruitment crisis are casting a long shadow. Hospitality remains fragile, and it will need sustained support and concessions from government in the months ahead if it is to help drive the UK’s economic recovery.”

Mark Sheehan, managing director at Coffer Corporate Leisure, said: “The June numbers are strong. Let’s not pretend that the road ahead is going to be smooth but what is clear is that consumers want to eat and drink out and the trend is upwards. This continues to be a difficult time, but optimism remains in the hospitality sector.

Paul Newman, head of leisure and hospitality at RSM, said: “June saw a strong return to restaurants and pubs as the heatwave early in the month encouraged many consumers to get out in the sunshine and socialise. The easing of restrictions later this month should provide more opportunities for get-togethers although it’s clear that a combination of Brexit, Covid restrictions and test and trace continue to have a huge impact on staffing availability. This squeeze in the labour market for a sector that is so heavily dependent on people is likely to dampen sales over the coming months. The finances of many operators remain on a knife-edge and the Government needs to consider a relaxation of visa barriers for hospitality workers to support the sector’s recovery.”

A total of 55 companies provided data to the latest edition of the Coffer CGA Business Tracker.

Participating companies receive a fuller detailed breakdown of monthly trading. To join the cohort, contact Andrew Dean at andrew.dean@cgastrategy.com.

About Coffer CGA Business Tracker

CGA collected sales figures directly from 55 out of the 61 leading companies participating. Participants include: All Star Lanes, Amber Taverns, Anglian Country Inns, Azzurri Group (Ask Italian, Zizzi), Banana Tree Restaurants, Beds and Bars, Big Table Group (Bella Italia, Las Iguanas), Boparan Restaurant Group (Carluccio’s, Gourmet Burger Kitchen), Bill’s Restaurants, BrewDog, Buzzworks Holdings Group, Byron, Coaching Inn Group, Cote Restaurants, Dominion Hospitality, Drake & Morgan, Fuller Smith & Turner, Gaucho Grill, Giggling Squid, Greene King (Chef & Brewer, Hungry Horse, Flaming Grill), Gusto Restaurants, Hall & Woodhouse, Hawthorn Leisure, Honest Burgers, Laine Pub Co, Le Bistrot Pierre, Liberation, Loungers, Marston’s, McMullen & Sons Ltd, Mitchells & Butlers (Harvester, Toby, Miller & Carter, All Bar One), Mowgli, Nando’s Restaurants, New World Trading Co, Oakman Inns, Peach Pubs, Pizza Express, Pizza Hut UK, Prezzo, Punch Pub Co, Rekom UK, Restaurant Group (Frankie & Bennys, Chiquitos, Brunning & Price), Revolution Bars, Riley’s, Rosa’s Thai, Snug Bar, Southern Wind Group (Fazenda), St Austell, Star Pubs & Bars, Stonegate Pub Co (Slug & Lettuce, Yates’, Walkabout, Bermondsey Pub Company), Tattu Manchester, TGI Fridays UK, The Alchemist, True North Brew Co, Upham Pub Co, Various Eateries (Strada, Coppa Club), Wagamama, Whitbread (Beefeater, Brewers Fayre, Table Table), YO! Sushi and Youngs.

About CGA:

CGA is the definitive On Premise measurement, insight and research consultancy that empowers the world’s most successful food and drink brands. With more than 30 years’ experience and best-in-class research, data and analytics, CGA is uniquely positioned to help On Premise businesses develop winning strategies for growth.

CGA works with food and beverage suppliers, consumer brand owners, wholesalers, government entities and pub, bar and restaurant retailers to protect and shape the future of the On Premise experience. Its mission is to use phenomenal data and expert insights to give brands a competitive edge and ensure the market we love is the most vibrant possible.

To learn more, visit: www.cgastrategy.com

Recent Reports:

- May’s total sales slip 26% at managed pubs, restaurants and bars as restrictions continue

- Sales down by a quarter at managed restaurants and pubs in April

- Christmas sales misery for pub and restaurant groups

- Drink-led pub and bar groups suffer 90% sales drop across November

- Tougher restrictions drive pub and restaurant group sales into reverse

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}