17 June 2022

Managed groups’ like-for-like sales flat in May as cost crisis deepens

Total Like For Like Sales Growth

- Restaurants in modest growth, pubs behind pre-COVID-19 levels

- London trading builds back, but dine-in dip shows fragile confidence

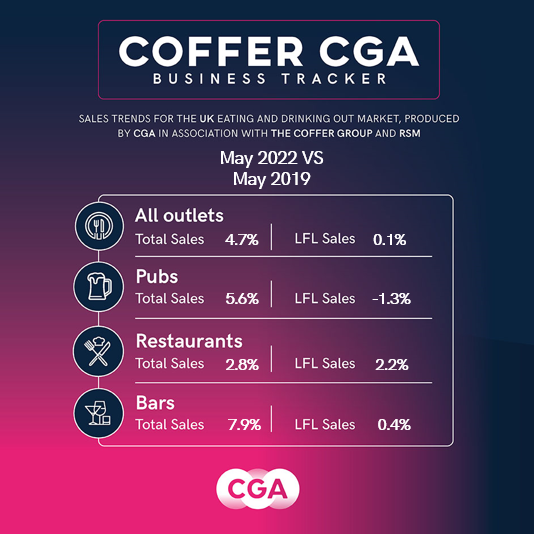

Like-for-like sales at Britain’s leading managed restaurant, pub and bar groups in May were just 0.1% ahead of the pre-COVID-19 levels of 2019, the latest Coffer CGA Business Tracker reveals.

The result from May’s Tracker—produced by CGA by NielsenIQ in partnership with The Coffer Group and RSM—follows like-for-like growth of between 2% and 4% from February to April. However, given high levels of inflation since 2019, sales are significantly behind pre-pandemic levels in real terms.

Comparisons are affected by the absence of the traditional late May Bank Holiday in 2022, after it was moved to June for the Queen’s Platinum Jubilee. This weakened trading against May 2019, which included two Bank Holiday Mondays. Nevertheless, given high levels of inflation over the last three years, sales clearly remain significantly behind pre-pandemic levels in real terms.

Restaurants recorded growth of 2% in May, while pubs were 1% down and bars were flat, the Tracker shows.

Trading in London improved in May, with like-for-like sales flat within the M25 as more workers and tourists returned to the capital. Sales outside the M25, which were well ahead of London for the first four months of the year, were also flat—a sign of a tightening squeeze on consumers’ spending in many regions.

The Tracker also highlights operators’ current reliance on delivery for sales growth. Dine-in only sales across all managed groups were 3% lower than in May 2019, while the CGA & Slerp Hospitality at Home Tracker—based on a different cohort of businesses—has shown that delivery sales have been four times higher than pre-COVID-19 levels in recent months.

Karl Chessell, director – hospitality operators and food, EMEA at CGA, said: “Managed restaurants, pubs and bars have shown impressive resilience since the start of the pandemic, and their appeal remains strong. However, rising costs in many areas are clearly tightening the squeeze on both operators’ profit margins and consumers’ discretionary spending. These all highlight that a number of challenges are likely to remain for the rest of 2022.”

Mark Sheehan, managing director at Coffer Corporate Leisure, said: “May like-for-likes were flat which with rising costs is a negative. June however should see a bounce with the jubilee and warmer weather and operators are optimistic for strong sales across the summer. The focus though is on staffing and rising costs. The issues with recruitment remain a critical problem for the hospitality sector.”

Paul Newman, head of leisure and hospitality at RSM UK, said: “It’s great to see London coming back to life with sales finally returning to a level not seen since the start of the pandemic, although the ability of operators to take advantage of this increased demand continues to be curtailed by significant staff shortages. With inbound travel corridors now fully open and the Jubilee weekend providing a showcase for pageantry in all its glory, operators will hope that these results finally herald the start of a sustained recovery led by international tourists helping to offset subdued domestic demand.”

CGA collected sales figures directly from 65 leading companies for the latest edition of the Coffer CGA Business Tracker.

Participating companies receive a fuller detailed breakdown of monthly trading. To join the cohort, contact Andrew Dean at andrew.dean@cgastrategy.com

About the Coffer CGA Business Tracker

Participants include: All Star Lanes, Amber Taverns, Anglian Country Inns, Azzurri Group (Ask Italian, Zizzi), Banana Tree Restaurants, Beds and Bars, Big Table Group (Bella Italia, Las Iguanas), Boparan Restaurant Group (Carluccio’s, Gourmet Burger Kitchen), Bill’s Restaurants, BrewDog, Buzzworks Holdings Group, Byron, Cityglen Pub Co, Coaching Inn Group Ltd, Cote Restaurants, Dishoom, Dominion Hospitality, Fuller Smith & Turner, Gaucho Grill, Giggling Squid, Greene King (Chef & Brewer, Hungry Horse, Flaming Grill), Gusto Restaurants, Hall & Woodhouse, Hawthorn Leisure, Honest Burgers, Junkyard Golf Club, Laine Pub Co, Le Bistrot Pierre, Liberation, Loungers, Marston’s, McMullen & Sons Ltd, Mitchells & Butlers (Harvester, Toby, Miller & Carter, All Bar One), Mowgli, Nando’s Restaurants, New World Trading Company, North Brewing Co, Oakman Inns, Peach Pubs, Pizza Express, Pizza Hut UK, Prezzo, Punch Pub Co, Rekom UK, Restaurant Group (Frankie & Bennys, Chiquitos, Brunning & Price), Revolution Bars, Riley’s, Rosa’s Thai, Snug Bar, Southern Wind Group (Fazenda), St Austell, Star Pubs & Bars, State of Play Hospitality, Stonegate Pub Co (Slug & Lettuce, Yates’, Walkabout, Bermondsey Pub Company), Tattu Manchester, TGI Fridays UK, The Alchemist, True North Brew Co, Upham Pub Co, Various Eateries (Strada, Coppa Club), Wagamama, Whitbread (Beefeater, Brewers Fayre, Table Table), YO! Sushi and Youngs.

About CGA:

CGA is the definitive On Premise measurement, insight and research consultancy that empowers the world’s most successful food and drink brands. With more than 30 years’ experience and best-in-class research, data and analytics, CGA is uniquely positioned to help On Premise businesses develop winning strategies for growth.

CGA works with food and beverage suppliers, consumer brand owners, wholesalers, government entities and pub, bar and restaurant retailers to protect and shape the future of the On Premise experience. Its mission is to use phenomenal data and expert insights to give brands a competitive edge and ensure the market we love is the most vibrant possible.

To learn more, visit: www.cgastrategy.com

Recent Reports:

- Managed groups’ like-for-like sales up 2% in April, but cost pressures stunt growth

- Managed groups’ like-for-like sales up 4% in March, but inflation holds down growth

- Managed groups’ grow like-for-like sales by 3% in February, but cost stresses mount

- Managed groups’ January sales up 3% on pre-COVID-19 levels as restrictions ease

- Managed groups’ December sales dip 11% as Omicron hit consumer confidence

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}